Financial Safety Guide

Hey Lykkers! Let's be honest—running a business is thrilling, but it comes with a lot of responsibility and risk. Even the most carefully planned ventures can hit rough patches, and suddenly, debts start piling up.

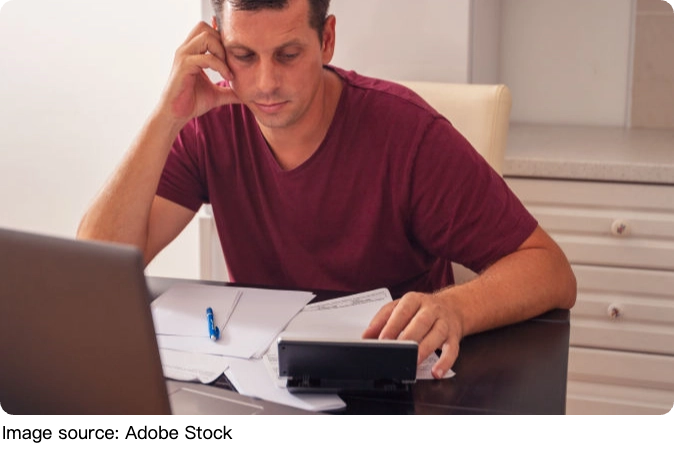

You're at your desk, sifting through overdue invoices and letters from creditors, wondering, "Could I lose everything I've worked for?" The good news is, it doesn't have to be that way.

With the right approach and a little strategic planning, you can protect your personal assets while handling business bankruptcy. In this guide, we'll walk you through actionable steps, legal tips, and practical strategies to safeguard your finances and come out stronger on the other side.

Understanding the Difference Between Personal and Business Assets

The first step in protecting your assets is understanding what counts as personal versus business property.

- Business Assets: These include office property, inventory, equipment, business bank accounts, and accounts receivable.

- Personal Assets: Your home, personal bank accounts, vehicles, retirement funds, and household belongings.

According to a 2022 study by the U.S. Small Business Administration, around 20% of small businesses fail in their first year, and nearly 50% fail within five years. Many failures are due to cash flow problems, and without proper planning, personal assets could be at risk if the business struggles. Recognizing the difference between personal and business property is essential for protecting what matters most.

Step 1: Choose the Right Business Structure

One of the most effective ways to protect personal assets is by selecting the right business structure:

- LLC or Corporation: These separate the business from the owner legally, protecting personal assets from most business debts. Over 70% of LLC owners reported reduced personal financial risk during times of business stress.

- Sole Proprietorship or Partnership: Here, the owner is personally liable for business debts, meaning personal property may be seized to satisfy business obligations.

It's crucial to consult a legal expert to choose the structure that fits your risk tolerance, business size, and future plans.

Step 2: Keep Personal and Business Finances Separate

Mixing personal and business finances is a common mistake that can lead courts to "pierce the corporate veil," making personal assets vulnerable. To prevent this:

- Open separate bank accounts for personal and business transactions.

- Avoid using business funds for personal expenses.

- Maintain accurate, detailed records of all income and expenditures.

Research shows that businesses with separate financial accounts are 60% less likely to see personal assets seized during financial distress. This simple step is one of the most effective ways to protect your personal property.

Step 3: Protect Key Personal Assets

Some personal assets are generally protected under the law, but rules vary by jurisdiction. Knowing which assets are shielded allows you to plan strategically:

- Retirement Accounts: Pensions, 401(k)s, and IRAs are often legally protected from creditors.

- Primary Residence: Many regions protect a portion of home equity, often ranging from $100,000 to $200,000 in the U.S.

- Insurance Policies: Certain life insurance cash values and annuities may be protected.

- Vehicles & Household Items: Most jurisdictions exempt vehicles and household items up to a certain value.

A licensed financial advisor can help you understand exemptions in your region and identify which assets you can legally protect.

Step 4: Avoid Fraudulent Transfers

While it's important to protect assets, never attempt to hide or transfer property unlawfully—it's considered fraud and can carry severe legal consequences, including fines and criminal charges.

Instead:

- Use legally sanctioned exemptions.

- Work with a professional on pre-bankruptcy planning.

- Keep all financial records transparent and accurate.

Transparency is key. Attempting to hide assets can not only nullify protections but may worsen your situation.

Step 5: Seek Professional Guidance

Bankruptcy laws are complex, and professional guidance can make a significant difference:

- A bankruptcy attorney can clarify which personal assets are protected and which debts are dischargeable.

- A financial advisor can help restructure debt, negotiate with creditors, and develop a post-bankruptcy recovery plan.

- According to the American Bankruptcy Institute, working with professionals increases the likelihood of a favorable outcome by 45–60%.

Investing in expert advice can save time, money, and unnecessary stress.

Step 6: Plan for Life After Bankruptcy

Bankruptcy is not the end—it's an opportunity to reset, reorganize, and rebuild:

- Rebuild savings and emergency funds (aim for 3–6 months of expenses).

- Monitor credit reports and work on improving your credit score.

- Implement strict financial controls to prevent future risks.

- Plan for steady growth, diversify income streams, and maintain clear separation between personal and business finances.

The Bottom Line

Lykkers, business bankruptcy can be intimidating, but with the right legal structure, financial separation, asset protection strategies, and professional guidance, you can navigate the process without risking your personal life.

Bankruptcy should be viewed as a strategic tool to reorganize debt, protect essential assets, and set yourself up for a stronger financial future.

By planning ahead and taking smart steps now, you can emerge financially stronger, more secure, and better prepared for future challenges.

-

Overcoming Money FearsStop Letting Social Media Steal Your Financial Confidence—Here's How!

Overcoming Money FearsStop Letting Social Media Steal Your Financial Confidence—Here's How! -

Tendinitis Syndrome Alerts!Is Your Joint Hurting More Than Usual? Spot Tendinitis Early And Prevent Serious Damage Fast!

Tendinitis Syndrome Alerts!Is Your Joint Hurting More Than Usual? Spot Tendinitis Early And Prevent Serious Damage Fast! -

UAE's Twin JewelsBeyond the Skyscrapers: Your Perfect Dubai & Abu Dhabi Adventure Awaits

UAE's Twin JewelsBeyond the Skyscrapers: Your Perfect Dubai & Abu Dhabi Adventure Awaits